Where MLO Referrals Die Before the Borrower Calls

Most loan officers measure referrals that call. They rarely measure the referred borrowers who search, feel uncertainty, and disappear before the first conversation.

Most MLOs think a referral dies because the borrower was not serious.

Sometimes that is true.

But a lot of referrals die in a quieter place.

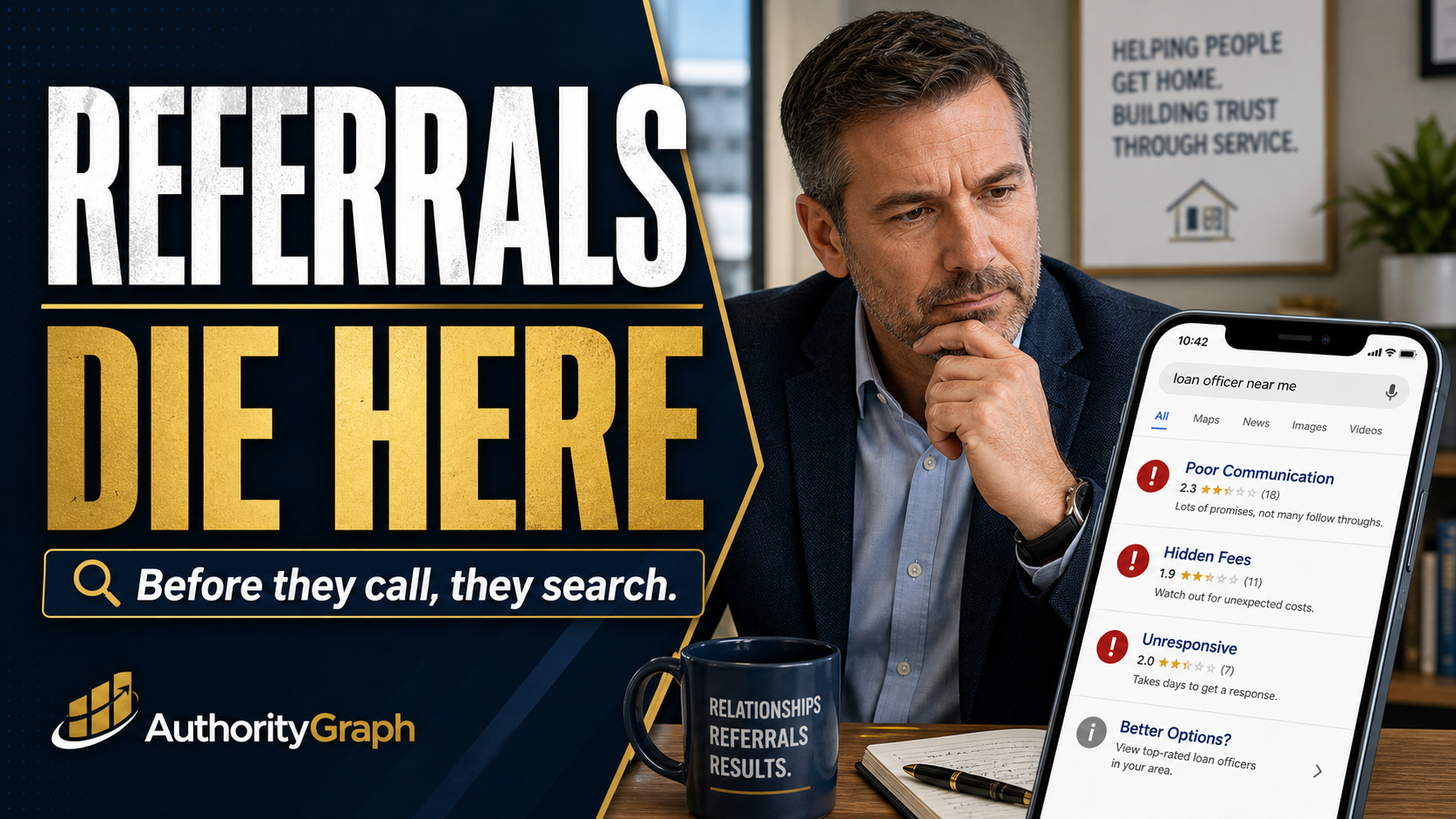

The borrower gets your name.

They search you.

They look at your Google result, LinkedIn, website, reviews, recent posts, and proof.

Something does not confirm the referral strongly enough.

So they never call.

No objection.

No we went another direction.

No chance to save it.

Just silence.

That is the part most loan officers are not measuring.

The referral is not the call

A referral creates attention.

It does not automatically create trust.

When a real estate agent, past client, CPA, attorney, builder, or financial advisor sends your name, the borrower usually has one immediate question:

Does this person look like the right person for me?

That question is answered before the call more often than most loan officers want to admit.

The borrower may not say it out loud. They may not tell the agent. They may not ask you a clarifying question.

They may simply search, compare, hesitate, and move on.

The leak happens between the name and the phone call

Most referral conversations are tracked after the borrower reaches out.

How many calls came in?

How many applications started?

How many pre-approvals moved?

How many files closed?

That scoreboard misses the invisible step.

How many borrowers were handed your name and never contacted you because the search result did not make the referral feel safe enough?

That is the referral leak.

It sits between the recommendation and the first conversation.

What the borrower checks

The borrower is not running a formal brand audit.

They are scanning.

They check whether the Google result is clearly you.

They check whether LinkedIn looks current.

They check whether your website explains who you help.

They look for reviews or proof.

They scan recent posts to see whether you are active.

They compare your public presence to the confidence of the person who referred you.

They ask, consciously or not, does this match what I was told?

If the answer is yes, the referral gets stronger.

If the answer is unclear, the borrower slows down.

Posting more is not always the fix

A lot of mortgage marketing advice starts with more activity.

Post more.

Make more reels.

Ask more agents.

Send more emails.

That can help, but it misses the first problem.

If the before-the-call layer is weak, more attention may only send more people into the same unclear search result.

The issue is not only whether borrowers hear your name.

The issue is what happens after they hear it.

The layer should answer seven questions

Before a borrower calls, your public presence should answer:

Who are you?

What kind of borrower do you help?

Why should someone trust you?

Are you active?

Are you specific?

Is there proof?

Is it easy to take the next step?

Those questions do not require hype.

They require clarity.

What this looks like for an average MLO

For an average loan officer, a stronger authority layer might mean:

- a LinkedIn headline that says more than mortgage loan officer

- a website or profile page that names the market and borrower type clearly

- reviews that are easy to find and consistent with the kind of work you want

- a simple page or article that answers a real borrower question

- recent activity that shows you are alive, current, and paying attention

- a contact path that does not make the borrower hunt

- the same story across Google, LinkedIn, website, and social

None of this is about pretending to be bigger than you are.

It is about making your real credibility easier to verify.

The practical test

Search your name the way a borrower would.

Then search your name plus your market.

Then search your company.

Then open your LinkedIn profile without editing it.

Ask:

Would a referred borrower know they found the right person?

Would they understand what kind of loan officer I am?

Would they see enough proof to feel safe calling?

Would they know what to do next?

If the answer is unclear, referrals may be leaking before you know they existed.

That is what AuthorityGraph is built to find.

Want to see whether your online presence is helping referrals convert or quietly leaking them? Request the free Before-the-Call Authority Audit.

Weekly observations like this one, delivered Tuesday morning. No fluff.